Curator’s Note: Stablecoins are slowly moving beyond crypto speculation, and becoming part of real financial infrastructure. This piece explores the growing divide between bearer stablecoins and bank-backed tokenized deposits, while showing how regulation, trust, and settlement efficiency may shape the next era of digital money. The real battle is no longer about crypto adoption. It is about who controls the future rails of global finance.

Stablecoins Are Becoming Something Much Bigger

A few years ago, stablecoins mostly lived inside crypto exchanges and trading platforms. Now the conversation feels very different. Big financial firms are starting to treat them like real payment infrastructure. Something that can move money faster, and with less friction than traditional banking systems. That change matters because the world is slowly entering a phase where money itself becomes programmable.

Some institutions believe bearer stablecoins are the future because they move openly across blockchains, without depending on intermediaries. Others believe tokenized bank deposits will dominate because regulators and banks already understand that structure more easily. And honestly, the entire financial industry now feels caught between speed, control, trust, and openness.

Why Bearer Stablecoins Feel So Different

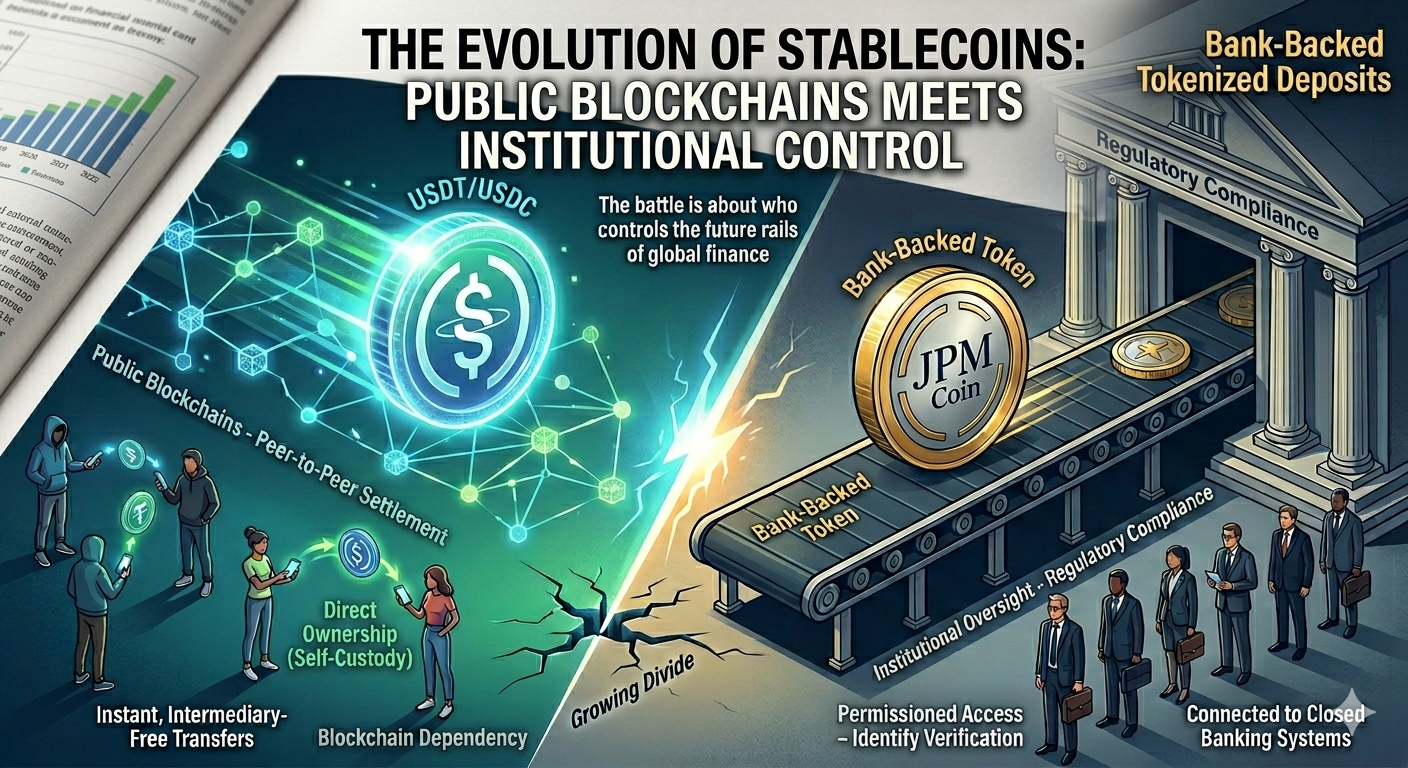

Traditional finance still depends on layers of intermediaries before settlement becomes final. Payments move slowly because institutions need time to verify ownership balances, and counterparty exposure. Bearer stablecoins change that structure almost completely. Ownership transfers directly onchain, and settlement happens almost instantly. That becomes extremely important as tokenized assets continue moving into blockchain systems. Stocks, bonds, and treasury products are slowly becoming digital instruments themselves. And once assets move at internet speed, the payment layer also needs to move with the same efficiency. That is why many institutions now see bearer stablecoins as more than crypto products. They are starting to look like infrastructure for the next generation of financial settlement.

Why Banks Still Prefer Tokenized Deposits

Banks are interested in blockchain technology, but they still want systems that preserve institutional oversight. That is one reason tokenized deposits are becoming attractive inside traditional finance. These systems keep banking relationships, and compliance structures connected to the movement of digital money. Regulators usually feel more comfortable with that model because the asset still behaves like a bank liability, instead of fully independent bearer cash.

But that structure creates friction as well. Transfers often require repeated permission checks, and identity verification before settlement can happen. Open interoperability becomes difficult because the system remains connected to closed financial environments. So tokenized deposits improve efficiency in some ways, but they still feel closer to banking infrastructure than internet-native money.

Stablecoins Are Changing Global Payments

Cross-border payments still feel outdated for many businesses around the world. International wires can take days, while fees continue reducing value across every transfer. Settlement also depends heavily on banking hours, and correspondent networks. Stablecoins remove many of those limitations because money can move almost instantly, at any time of the day.

That is why payment companies, treasury teams, and financial networks are paying serious attention now. What makes this transition interesting is that stablecoins are not replacing old payment systems overnight. Instead they are slowly entering the settlement layer underneath existing infrastructure. That pattern happens often during technological transitions because old systems usually remain visible, while new systems gradually begin carrying the real operational load.

Regulation Is Slowly Defining The Future

Governments now understand that stablecoins are becoming too important to remain in a regulatory gray area. Europe introduced MiCA with strict reserve requirements, and redemption protections for digital fiat issuers. The United States followed through the GENIUS Act, and created clearer legal standards around reserve backing, and issuer supervision.

That clarity changed institutional sentiment very quickly because large financial firms do not move serious capital into uncertain environments. Stablecoins are now moving closer to mainstream finance, and further away from their earlier experimental image. Regulators are basically deciding which type of digital money can become trusted enough for global adoption. And honestly, that decision may influence financial systems for decades ahead.

Trust Will Probably Decide Everything

Technology alone will not decide which stablecoin model survives in the long run. Trust will matter much more than innovation. Bearer stablecoins create incredible settlement efficiency, but they also create dependency on reserve transparency, and redemption confidence. If a major issuer fails during large redemption pressure, the effects could spread very quickly across connected markets.

That is why institutions are demanding stronger Proof of Reserves systems, and clearer custody protections. They want proof that backing assets truly exist, and remain accessible during financial stress. Financial systems often look stable while markets remain calm. The real pressure always appears when confidence weakens, and large numbers of people suddenly demand liquidity at the same time.

The Real Fight Is About Financial Infrastructure

A lot of people still frame stablecoins as a crypto industry topic, but the situation has become much larger than that now. What we are really watching is a battle over the future architecture of global finance. Bearer stablecoins offer open interoperability, and internet-level movement of value. Tokenized deposits offer tighter institutional alignment, and stronger regulatory familiarity.

Both systems are trying to become the foundation for how digital money moves across the world in the coming decades. And whichever structure wins will likely shape much more than payments alone. It could influence sovereign debt markets, corporate treasury systems, global trade flows, and even how ordinary people experience money in everyday life.

Hamid Akhtar

hmdlabee@gmail.com

Leave a Reply